Advance rulings was introduced by the Finance Act,1993. Chapter XIX-B (Section 245N to 245V) of the Income-tax Act, which deals with advance rulings, came into force with effect from 1-6-1993.

What is advance ruling?

“Advance Ruling is a more or less a binding statement from the revenue authorities upon the voluntary request of a person, concerning the treatment and consequence of one or series of future actions or transactions.”

Simplification of Reason to introduce the concept of Advance ruling

In a simple term advance tax ruling is a written interpretation of tax laws. It is issued by tax authorities to corporations and individuals who request for clarification of certain tax matters. An advance ruling is often requested when the taxpayer is confused and uncertain about certain provisions. Under Income Tax advance ruling is available in International Taxation.

It helps foreign investors in determining their tax liabilities in advance so that they can assess the transaction that they propose to undertake.

It also brings certainty in determining the tax liability, as the ruling given by the Authority for Advance Ruling is binding on the applicant as well as Government authorities.

Why is advance ruling under Income-Tax necessary?

- Provide certainty for tax liability in advance in relation to a future activity to be undertaken by the applicant

- Reduce litigation and costly legal disputes

- Attract Foreign Direct Investment (FDI) – By clarifying taxation and showing a clear picture of the future tax liability of the FDI.

- Rulings are binding on the applicant as well as the department.

Transactions on which taxpayer can request for advance ruling under Income-Tax

Any taxpayer can request for advance ruling when he is uncertain of the provisions. Advance tax ruling is a determination or decision by the authority in relation/respect;

(i) To a transaction which has been undertaken or is proposed to be undertaken by a non-resident applicant; or

(ii) To the tax liability of a non-resident arising out of a transaction which has been undertaken or is proposed to be undertaken by a resident applicant with such non-resident; or

(iia) To the tax liability of a resident applicant, arising out of a transaction which has been undertaken or is proposed to be undertaken by such applicant;

and such determination shall include the determination of any question of law or of fact specified in the application;

(iii) Of an issue relating to computation of total income which is pending before any income-tax authority or the Appellate Tribunal and such determination or decision shall include the determination or decision of any question of law or of fact relating to such computation of total income specified in the application;

(iv) Whether an arrangement, which is proposed to be undertaken by any person being a resident or a non-resident, is an impermissible avoidance arrangement as referred to in Chapter X-A or not:S

Provided that where an advance ruling has been pronounced, before the date on which the Finance Act, 2003 receives the assent of the President, by the Authority in respect of an application by a resident applicant referred to in sub-clause (ii) of this clause as it stood immediately before such date, such ruling shall be binding on the persons specified in section 245S

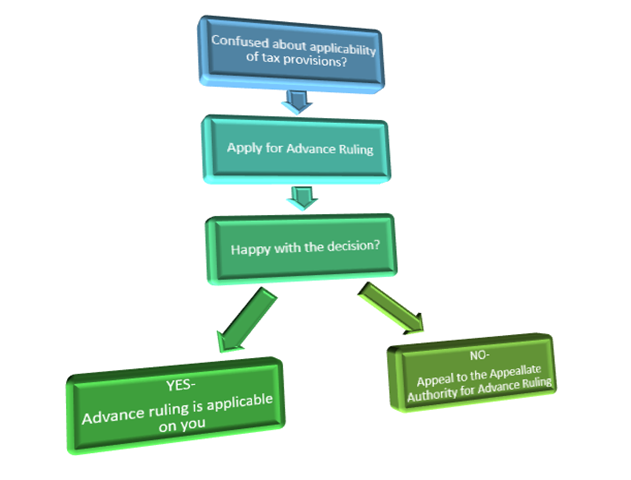

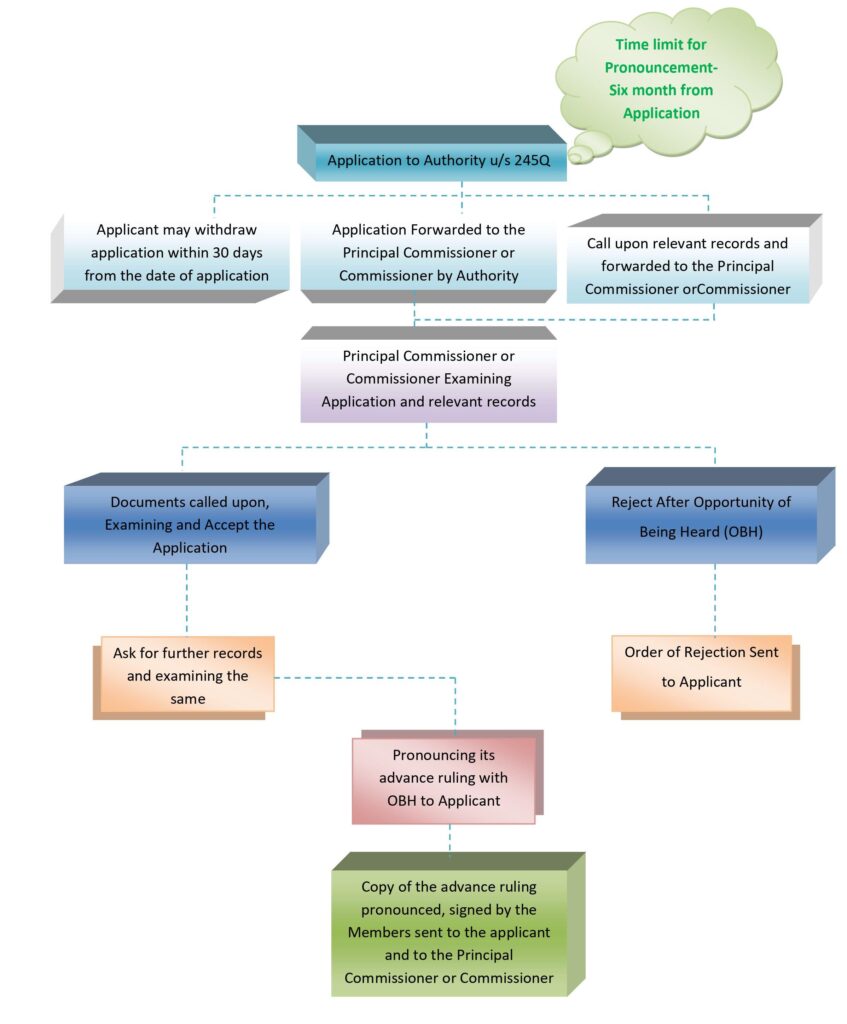

Procedure on receipt of application

Appeal to the Appellate Authority